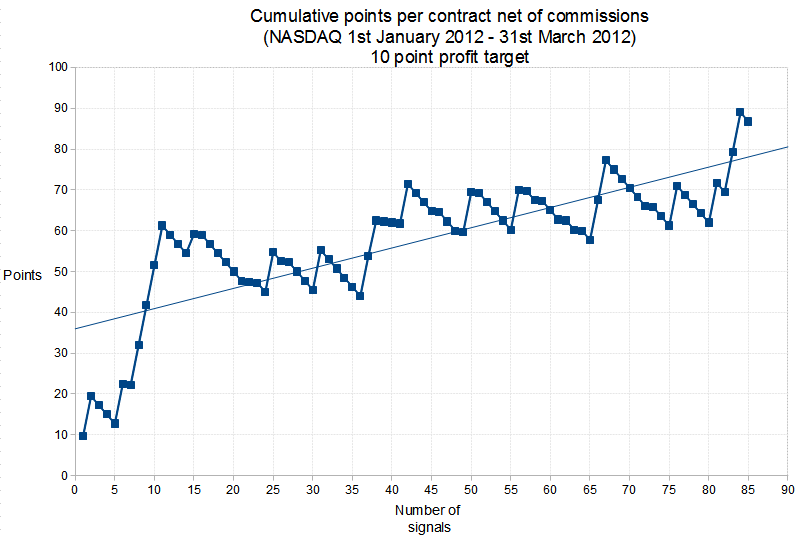

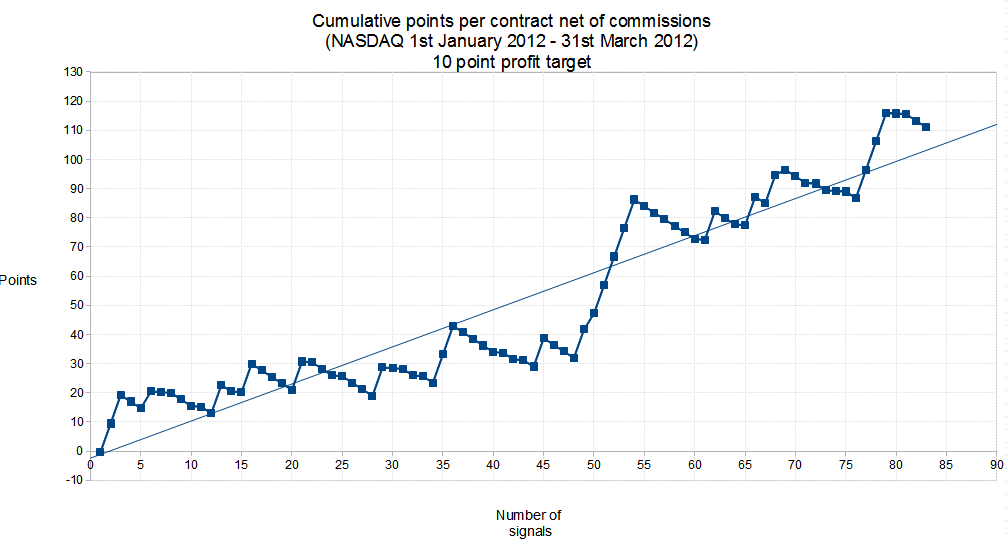

Each of them are based on different indicators I've come up with. The data used was from 3rd January 2012 to 31st March 2012.

The first strategy results (based on a derivative of my PDI indicator);

The second strategy results (using a $ Index based indicator);

The results from the first one here really are not good, average gain per trade is just one point, completely invalidates that indicator.

The results from the second are slightly improved but not by much, suggests there is slightly more merit to the indicator used for that one but again it wouldn't be smart to trade it when you know before you start the average yield per trade is going to be low.

Still, this is the point of backtesting.

I'll need to come up with something completely new and original.

No comments:

Post a Comment