There's been some tumbleweed blowing through this way of late.

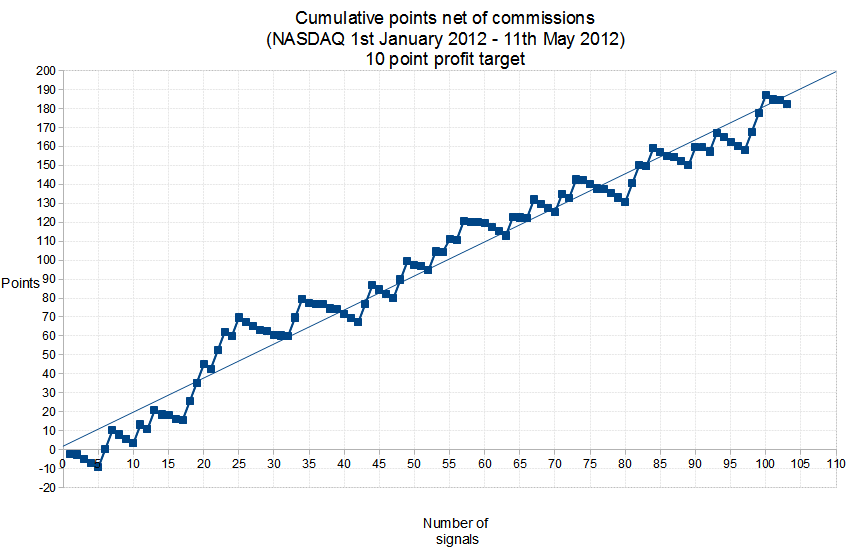

I've been backtesting a different trading strategy, looking at data from 1st Jan to 11th May this year. It's using a combination of two indicators I developed, working together, each acting as a filter for the other.

Trading strategy II

At first, I wasn't particularly impressed with this, on the other hand, based on the period studied, it looks consistent, and that's a useful trait if that replicates when I trade it.

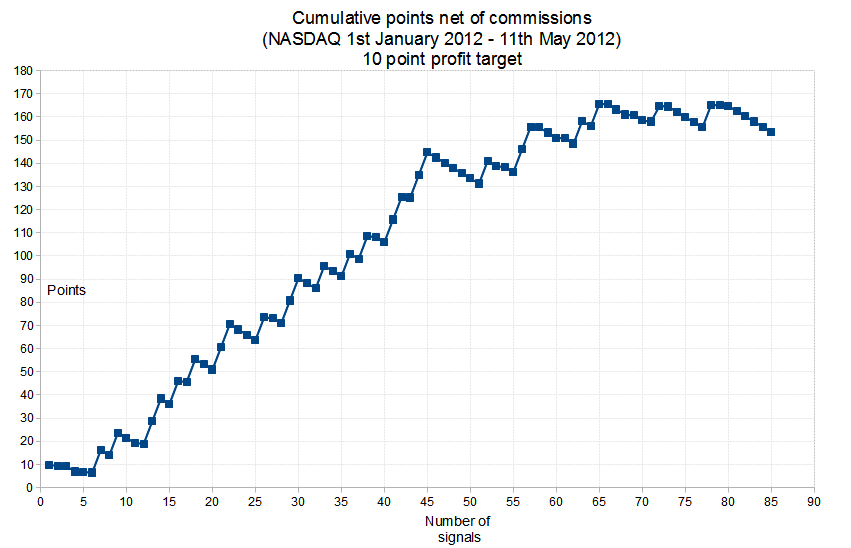

What I also looked at, was the relationship between the results and the time each signal was given. In order to test this I reordered the signals given from the data range, to list signals in time order during the day, then charted them. So each subsequent signal of the next chart occured at a time later on during any given trading day.

Trading strategy II (Signals sorted by time - earliest first)

Signals from 7 to 45 represent 2pm to 4pm (UK time), and are clearly more favourable then after 4 pm. After 4pm the signals become less consistent.

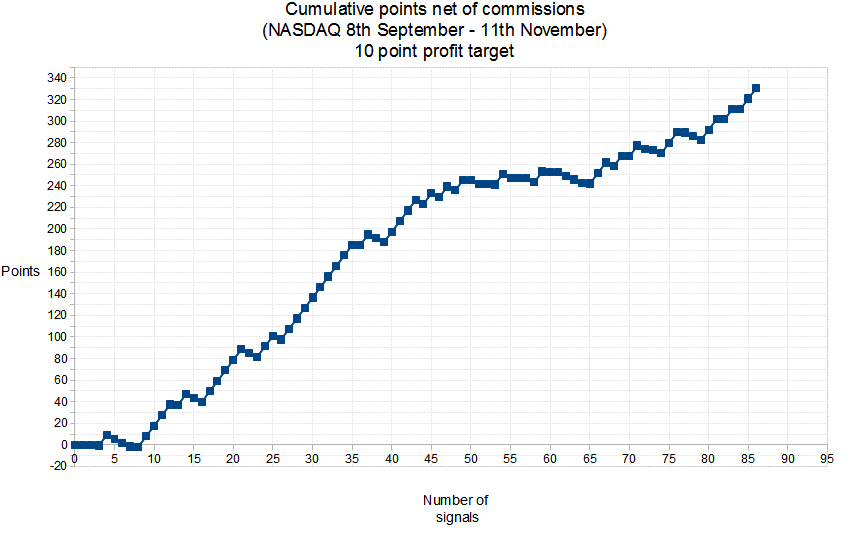

What I also did was to look at previous test data for the previous trading strategy in exactly the same way, to see if the same type of result would be found (signals occuring between 2pm and 4pm (UK time) providing more favourable trading results);

Trading strategy I (Signals sorted by time - earliest first)

Broadly the same pattern is found, signals 5 to 43 represent 2pm to 5pm, so again the US morning session provides the most favourable period to trade, based on both strategies.

I start trading Strategy II from next week, although trading may be sporadic since I'll be married by then and may have to pay some attention to my newly minted wife.

No comments:

Post a Comment